The Fed is now firmly committed publicly to a very aggressive rate hike cycle in 2022 and possibly into 2023. It started with the now erstwhile hawks on the FOMC who all got pushed out during last year’s ‘insider trading’ scandal.

It’s continuing today as FOMC Chair Jerome Powell, almost immediately after the ink was dry on March’s anemic 25 basis point raise began ratcheting up the hawk talk in a clear signal to markets that seven quarter-point raises this year won’t be nearly enough to restore the Fed’s credibility with capital markets.

All last year I kept telling you that there was a major internal battle happening for control over the Fed in order to stop the ‘policy error’ of raising rates into a supply-constrained cost-push inflation cycle.

I won’t rehash all the twists and turns of this story today because the fact that we are here with Powell as Chair pro-tem, still awaiting a proper confirmation hearing is the one thing you need to know that proves that correct. The Democrats continue pushing outright communists onto the FOMC board like Sarah Bloom-Raskin to replace the scalps taken last fall to forestall Powell’s actual confirmation.

Powell absolutely wants to make Monetary Policy American Again, after fifty years of Eurodollar markets setting monetary policy for them. As Jeff Snider so painstakingly has proven to us, the Eurodollar system is more powerful than the Fed in creating dollars and pricing the risk of those new dollars.

With a sympatico Congress that never met a spending bill it couldn’t compromise it’s way to betraying the American people with, for decades we’ve seen nothing but rearguard actions by the Fed when it tried to normalize interest rates.

The failure to pass Build Back Better was the watershed moment for us here in the US. Without it, a Powell-led Fed was free to eventually end QE and begin raising rates. It needed time in 2021 for the inflation narrative to outrun the COVID-19 narrative. Once the latter ended the political support for BBB vanished and Powell was free to begin the tightening cycle.

Because we’ve been so conditioned to the Fed caving in the past we’ve come to expect it as de rigeur they will cave again. This is why there was so much disbelief leading up to the March meeting that the Fed would actually raise rates.

The typical Austro-libertarian analysis is, unfortunately, as brain dead as it is dead right, in theory. For a taste of it I refer you to the podcast I did recently with Peter Boockvar. But you’ll hear similar analysis from Peter Schiff and his stable of writers.

I don’t disagree that the Fed is facing unpalatable choices. The Fed is trapped along certain vectors. It can’t raise rates without causing a recession or destroying the yield curve.

So, they argue, the Fed will have to reverse any rate hikes because if they don’t it will blow up credit markets and then be blamed for killing the golden goose. Politically, it’s always a non-starter. So, the Fed will raise rates and then give them all back.

At what point will that happen? 1% on the Fed Funds? 1.5%? 3%?

But there are a number of underlying assumptions in that conclusion that may no longer be accurate.

And it is these assumptions that have led me to consider what if the Fed isn’t operating based on the same metrics of the previous cycles?

If you reject that outright, you get Mr. Boockvar’s or Mr. Schiff’s take. It’s the safe conclusion. It’s based on past behavior.

But is it based on the current market conditions?

I don’t think so. In fact, I’ve come to the conclusion that nothing about the current state of affairs politically, economically or militarily are anywhere close to similar to where we were in early 2019 when the Fed followed the ECB in cutting rates because their markets became unstable.

I’ve written extensively that I felt the Fed began tightening last June with their raising the payout rate on reverse repos to a measly 0.05%. This had the momentous effect of crashing the euro 3% in a day while Biden pushed confrontation with Russia over Ukraine out for another eight months in Geneva when he met with Putin.

It ended any thought of a bull market in the euro versus the US dollar.

So, while I’ve been arguing for a while that the Fed has been in tightening mode for months, the thing that eluded me was how were they going to pull that off without a repeat of past performances?

The underlying assumption for this is that the Fed, as an advocate for U.S. commercial banking interests, is engineering a split with the Eurodollar system which has now reached the end of its ‘use-by’ date, given the dire fiscal circumstances the U.S. finds itself in.

Moreover, I’m further postulating, and I think with good reason, that the Biden Administration and most of the leaders in Congress do not work for American interests, but the opposite. It is the only realistic explanation for their behavior, especially since the beginning of Russia’s war with Ukraine.

So if Biden et.al. works for Davos and Davos wants an end to U.S. commercial banking dominance, then it makes sense they would need control over the Fed to pull off their move to central bank digital currencies (CBDCs) and create the apotheosis of the Great Reset.

Under those conditions the Fed would absolutely act ‘out of character,’ leaning into the ‘policy mistake’ of raising rates into a stagflationary environment with US debt to GDP at 109%.

Again, the problem arises, the minute the Fed goes hawkish they will have to reverse themselves quickly lest they torch the global credit markets.

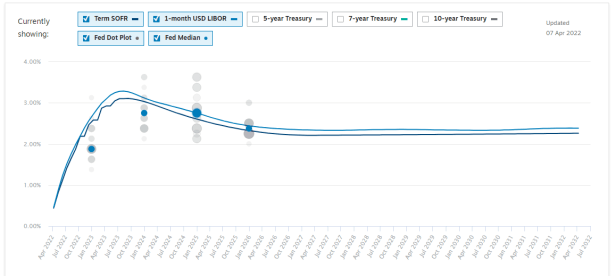

And this is where I think SOFR plays a big role in destroying the thesis that the Fed is trapped in the same way that it has been in times past.

What is SOFR? The Secured Overnight Funding Rate. It is the U.S. domestic replacement for LIBOR. SOFR is market driven arrived at through actual transactions in the U.S. money markets with the daily quote arrived at by real data from real US banks.

LIBOR, on the other hand, is a rate set by 17 foreign banks and 1 U.S. bank (JP Morgan Chase’s London Division). It’s still not market driven but arrived at by consensus. Regardless of that it represents the activity within London’s and Europe’s banking system, not the U.S.’s.

And therein lies the rub.

For all intents and purposes for decades LIBOR was the mechanism by which City of London and Europe controlled the flow of dollars into and out of their banking system. No wonder the Fed had no real control.

Broadly speaking, when the Fed raises rates and it causes a drain on the eurodollar system, it puts upward pressure on LIBOR. If Europe’s banks are more exposed to a rise in the cost of dollars then LIBOR should blow out faster than the Fed raises rates.

In past cycles, before SOFR, all US debt was indexed to LIBOR. So, it didn’t matter if the Fed raised rates domestically, our mortgages, lease rates, and credit lines blew out with LIBOR even if there was no underlying stress in these domestic markets.

Now, in 2022, with all US debt indexed to SOFR and almost all legacy debt reindexed to it over the past four years, when the Fed raises rates U.S. debt rates rise with it, rather than with LIBOR. In short, SOFR breaks the link where Europe or London’s problems cross the pond and become our problems.

It leaves them free to pursue insane monetary policy like, say, negative nominal rates, for a full decade but can no longer force the U.S., in effect, to fund it.

As the Fed raises rates this summer the possibility exists that SOFR insulates the US from the havoc that the draining of eurodollar markets will have on LIBOR-indexed debt.

Remember also that the SOFR crisis of 2019 was due to the U.S. markets running out of cash caused by U.S. banks refusing to take European debt as collateral for repos throughout the year. It forced the Fed to open up the repo window to provide that cash and alleviate the problem in the short term.

This is a clear ‘shot across the bow’ from US commercial banks saying they were done financing Europe’s debt orgy. The battle lines, I think, were drawn in 2019 and the next phase of the battle is on the table today now that Powell and company have a fully realized SOFR market operating in all areas of U.S. debt markets.

This is what has changed. This is one more weapon in the Fed’s arsenal to wrest control over U.S. policy, both fiscal and monetary, that it can use to assert its independence and put the U.S. back on something close to a sustainable path.

Europe, on the other hand, can no longer count on their controlling LIBOR to get the dollars they need from either a willing Congress and a trapped or captured Fed.

Moreover, if you really begin to think through this, again in broad terms, it puts the new pricing system for commodities thanks to the Russians, i.e. rubles = gold = oil = commodities, on the other side of Europe saying in no uncertain terms #GotGoldOrRubles?

And they can’t print the same number of eurodollars they used to. So, now what?

This is where we are today. I laid out this whole thing in a recent interview with Chris Marcus at Arcadia Economics.

I’m not saying in any way that what I’ve outlined here is the only new fulcrum on which the future of financial markets rest. That would be ridiculously arrogant.

But I am saying, as always, that if you don’t constantly challenge your assumptions about how things work and what the motivations are of the people who operate these systems then you are likely to make a foundational mistake about where we are headed.

Because how else do you explain the Fed so rapidly reversing course on ‘inflation is transitory’ to ‘inflation requires extreme measures’ to the point where uber-dove and MMT fan girl, Lael Brainard is now talking the hawkish talk?

What if the goal of this FOMC is bigger than just the normal steering us through a difficult time? What if this time it is the Mises Crack-Up Boom and the old alliances are gone and it’s now an all-out Hobbesian war of “all against all” not only geopolitically but financially as well?

What if the Fed’s upcoming ‘policy error’ is nothing of the sort but a sincere attack on its biggest enemies?

Under those circumstances anything is possible. And if you aren’t willing to reframe the current conflicts along the proper lines, I would remind you of what Ayn Rand would say, “Check your premises.”

Join my Patreon if you hate LIBOR

If you watched Biden snubbed by Obama and Harris yesterday, it is obvious that they want sleepy Joe to be removed from office asap. He doesn’t do anything in terms of committing US army against Russians and he keeps Powell. Now the question is whether Powell is the real target?

Yes

Biden is about done. When I use the term “Biden” anything… I mean Obama.

What is the master plan? Fed kills the Euro – Nato kills Europe and Russia by having them go kinetic on each other. As a result, the Belt & Road dies and China is crushed because it loses Europe as a buyer of its crap and becomes solely dependent on the US consumer while China gets isolated in East Asia leaving the US as the strongest man standing?

They are ambitious I’ll give them that.

There is no grand plan anymore…just a lot of people running around trying to stay relevant

I was kind of assuming that there remains a grand plan but a truck load of unintended consequences, in which Russia and China get the biggest votes.

Incidentally, how does your thesis dovetail, or not, with Hudson’s Dollar Devours the Euro article over at the Saker?

I’m not sure these cockroaches have scattered yet and started turning on each for survival. If we are counting on the likes of Jamie Dimon to be our saviour in the fight against the globalists then God have mercy on us.

Sometimes its hard not to slip into the “everything is planned accordingly” mindset. I do it all the damn time. But I think the correct call on this is the one you just made. Why? Because the way the media has been behaving since this started. There is a frantic atmosphere about it. I don’t consume much mass media but I can sense it. This tells me they are scared this is going to get out of control. When I say I mean Davos who orders the media to spread the narrative.

“Join my Patreon if you hate Libor” — love that! (sovereigns only:)

Sovereign men only

Hi Tom, great article and video. I was not aware the LIBOR was a continuation of the Eurodollar Market which London set up in the late 50’s and killed Bretton Woods in 1971

See article and film below

Best regards

Stuart, Cairns

Australia

https://citizensparty.org.au/sites/default/files/2019-08/euromarket.pdf

https://www.bitchute.com/video/1lYVrv3tQVIH/ – ‘The Spider’s Web – Britain’s 2nd Empire’

You know Tom, it occurs to me that Russia has killed the petrodollar which was how the US exported inflation to the rest of the world. Every other nation that attempted to sell oil for anything other than dollars got itself bombed into oblivion. That simply won’t happen with Russia.

The Eurodollar mechanism for exporting inflation now becomes a liability rather than an asset because there is no reason for needing large amounts of dollars in the rest of the world in the future. It seems likely that even the dovish members of the Fed understand what this means.

The only reason this looks like a policy error to the Schiff crowd is because they are looking at this as strictly an economic problem. They are not considering the geopolitical interests of those running the Fed. They will be right about the economic effects of raising interest rates but that is beside the point for those who run the Federal Reserve.

I’ve wondered whether massive loss-making enterprises like the US shale industry, SpaceX and TESLA are actually heatsinks for the dollar to compensate for its declining use abroad, allowing dollars to be printed but sequestered?

Might explain why Musk is untouchable?

That’s a great thesis. I’ve been thinking lots lately about Musk, and his role. He has been chosen for a role, just like our comedian friend.

There will be a lot of dollars flooding America soon

Peter Schiff correctly called Powell’s renomination. His reasoning was that if Brainard was nominated instead, then Brainard and by association Biden could be blamed for the inevitable economic shitstorm that is heading our way. At least when said shitstorm happens more blame can be shifted to Powell and by association Trump etc. The devil you know is better than the devil you don’t.

This is how I see the bad ending playing out. FED raises rates, we get a biblical economic meltdown. But instead of customary bail outs, banks get bailed in allowing for the general populace to be chained to the resulting change in monetary policy that has been created by our technocratic overlords beforehand.

Russia and China who have been preparing for this outcome and who are insulated by commodities come out the least unscathed. China because of their absolute bending over to Davos, becomes the shining light of the world with their digital technocratic state by which the west will be encouraged to model itself by.

Covid and Russia are blamed for the global meltdown. Life carries on thanks to some kind of SDR digital currency made up of a basket of currencies provided for by the IMF. Davos agenda becomes instituted as the impetus for the 4th industrial revolution. A type of cold war 2.0 between East and West heats up. Technological arms race for robots and drones also heats up.

The U.S segregates into an even wider dichotomy. Gun, gold, and goat loving constitutionalists who try to rebel are shot out of the sky by drones. The U.S constitution becomes abolished. And culling of the global population at large accelerates. Be it by food crisis and or disease. I suspect another much deadlier bio-engineered virus will be released some time down the road at an appropriate time. Except this one will target the non-compliant unvaccinated types thus further incentivizing vaccines, vaccines which perhaps work but with population reducing effects that have been fine tuned. Of course, the more important managerial class of the Davos crowd won’t have to worry about the vaccines designed for them.

The end.

Are all of these guys on someone’s payroll? There has got to be ten profiles writing this same sort of boring SciFi on every article. Is it the same guy?

“I’ll be back.”

Pretty much bang on target in all respects. Although I think the Fed is just talking tough because they know a cyberattack is coming (blamed on Putin) to cause the meltdown and they need to have credibility in the aftermath.

I think the reason the Davosians have worked so hard to engineer such extreme societal division in America is because it’s the only remaining nation with large numbers of armed patriots.

And the Davosians can now fight them down to the last progressive Millennial.

Yeah, this cyber attack is just around the corner.

Agreed.

Wow…that was a mouthful. Nice imagination…vivid, but not realistic.

“how else do you explain the Fed so rapidly reversing course on ‘inflation is transitory’ to ‘inflation requires extreme measures’”?

They have a scapegoat now.

The inflation created by the Fed was benign. The inflation being created by Putin is malevolent.

So now they get to claim they are monetary heroes fighting the Putin Price Hikes.

If a controlled demolition of the world’s monetary system is underway, who will we turn to in the aftermath?

Monetary heroes.

“Do you feel in charge?…This gives you, power over me?…Your money…has been important, until now…I’m…here to end to the borrowed time you’ve all been living on…I’m necessary evil.”

Sums it all up perfectly. LOL

Tom,

I am not up on economics, but your whole LIBOR verses SOFR thesis has a familiar historical ring / overtone to it.

As Americans we were all taught that the American Revolution was about a fairness issue: “No Taxation without Representation”. It seems like such a reasonable and small thing to ask and paints the British Crown as unreasonable and tyrannical. However, we are never taught is that it was really an “impossible ask”. Just think deeply about what would have happened if it were granted? It was all about “REPRESENTATION” …if the British allowed popular representation, then they would have created a power inversion in the Empire. As soon as they got to the point where there were more people living in the colonies than in the British islands, the Empire would become governed from Philadelphia, not London.

And it was this issue that made the Spanish Empire impossible to reassemble after Napoleon smashed it in 1807 in the Peninsular War. They based reassembly around popular sovereignty and discovered that there were more subjects living abroad than there were living in Spain. So, popular sovereignty would have effectively made Spain a colony of the colonies. Caracalla made a similar mistake when he granted all freemen Roman citizenship, thinking it would bring the Empire together, when in actuality, it did the reverse. After Caracalla’s edict, Rome was no longer at the center, the regions were.

So, the whole LIBOR verse SOFR thesis has a familiar historical ring to it. What happens where there are more US Dollars outside the United States than inside the United States? And that may be the overall macroscopic issue driving all of this? All of it. It is a really ingenious discovery on your part. IMHO

I just thought I would point this out as you formulate and strengthen your argument.

And thanks again for a really thoughtful essay. This blog is amazing; I think you and Dexter are well ahead of your peers!

The American colonies got their “representation” and then quickly got a higher tax from their new government than they were previously paying to the crown. So some of them rebelled until Washington sent in the troops. Meet the new tyrant, worse than the old tyrant.

Lewfalo:

The point that I was trying to make was to another set of Inside v. Outside money; apart from Pozar’s commodity-based v. financialized money. So, if you imagine yourself in Italy, during the Roman Empire, and money “flowing to where it is treated best”, the best place for money was on the outskirts of the Empire. And this would be reflected in the Roman elites, who, because they were investing in the provinces would adopt a more global perspective to the Roman Empire, than the non-wealthy classes living on the Italian Peninsula. And so, over time, an anisotropy developed in the Empire between the traditional center of power and borders (ie the extant governing structure) versus the real economy, which was centered in the provinces. So, I am guessing something similar happened back then as is now happening in the United States. The population that was connected to the border (globalized) economy was doing better than the peninsular (national) economy. And the folks stuck in Italy, would be saying things like, “make Rome great again” verses the other class who saw their future away from the peninsula. So, you would get a national verses globalist split. Thus, the LIBOR/WEF faction of financiers is acting in much the same way as the Roman pro-provincial faction. And so, while the LIBOR and SOFR factions are battling it out, the Russians, Chinese and other former satellites of the Anglo-American Empire are saying we want out of the system all together.

I was not really trying pick a side, whether the colonies were better or worse off as independent, but to further develop Tom’s thesis. At the height of the Roman Empire, there was probably a few types like Francis Fukuyama that predicted the “end of history”, while in reality the Empire that they thought was so solid, was coming apart, due the anisotropy I outlined above.

If I am biased it is probably because I cynically believe that there are inescapable natural laws and cycles that govern human behavior, like “money flows to where it is treated best” and “money is tokenized energy” verses believing that we have entered into a new, woke, progressive era, espoused by Barack Obama, etal. They seem to have forgotten that it was only 80 years ago that we were dropping atomic bombs and rounding up entire populations in genocidal pogroms… and what has really changed? …that we all now have laptops, iPhones and social media accounts?

This is a very interesting perspective on this LIBOR/SOFR issue, AnonX. I would say that LIBOR was always the way for the old European powers to keep the colonies under their ultimate leash while they pursued their wars for profit. Both WWI and WWII can be thought of as wars they fomented while they hid their money in the US away from the conflict.

Then when the war was over, WWII, they left in place a typical British poison pill which eroded any power the US gained from being the only one left standing to rebuild their power base via the Marshall Plan while undermining the Fed’s growing dominance.

It’s one way of looking at it.

Tom, It could be. I am going to have really do more reading on economic, banking and financial history to further my understanding. I had a similar career path as yourself, but with a second major in history instead of English. I used to think of history as pretty cut and dried, but now I have to give it a lot more respect. Just as I would not walk into a chemistry lab and start blithely mixing solutions, I feel almost the same about history now, including taking a position about anything in current events. If the United States and the City of London were temporary refuges, I just wonder where they plan on escape to next? …as it seems they have run out of countries. Anyway, thanks again for your LIBOR v. SOFR analysis, I think it is on the right track and offers a lot to think about.

For me history became more interesting when I realized that you have to incorporate economic analysis into how events unfold

Tom: Addendum. I think the difference between our 2 points of view is that I was looking at WWI & WII as European screw-ups, which caused the Europeans to take refugee in America and the American bankers to take advantage of the Europeans. So, I was saw the WEF/Davos effort as an attempt to shift the locus of power back to Europe, because (as you explained to us) the Eurodollar market is now so big. (?) That is sort of how I viewed Dr. Strangelove… as Kubrick saying we (the British Empire) just defeated the Nazi’s but inexplicably the reckless Americans have invited them over and now they are back to prosecuting their war against Russia, this time with nuclear weapons. Kubrick gave me the impression that the European’s / Brits viewed themselves as horrified bystanders between the ill-bred Americans and the crackpot Marxists.

And so, seeing the WEF/Davos crowd getting squeezed between the Fed and the commodity backed currency nations was a bit of schadenfreude on my part.

However, I will take into consideration your POV, that they may have been in control all along… it is something I had not considered before, but I am open to it, as I do more reading.

Cool. There’s a lot of work out there positing that perspective. But that’s a really interesting take on Dr.Strangelove. I hadn’t thought about it that way at all. Thanks

Thank you for your contribution to this community. Tom has written an amazing essay and you have helped make the discussion of the topic even more brilliant!

Thanks. I am amazed by GG&G too. What is even more ironic is that I have close to ZERO interest in finance, I guess because I am surrounded by people who are obsessed with it. I am sure they would be shocked to learn that I am reading a financial blog. (lol) But I think Tom & Dexter’s stuff goes way beyond how to make money on Gold ETFs and Bitcoin. Way beyond…

*The one financially related thing I did do, after reading GG&G, was to buy 3 years’ worth of nitrogen-based fertilizer for our garden. I was questioned for doing it then, but now others around me think I am some kind of Nostradamus as they see the sacks of urea in our garage and note the current prices. (lol)

What do youake of the RCB changing the gold peg? Did the Ruble rise faster than they expected or is Elvira being a dumb bitch again?

Tom is expecting the RCB to be nationalized soon I think.

The former. Nabiullina was forced to lower rates because ruble demand was so high that she had to loosen things up to reflect demand. This is a good sign, it shows the IMF argument of linearity between rates and inflation and rates vs. demand are invalid.

Remember, Keynesian economics is bullshit as are all things Malthusian. This is their Achilles heel, using linear models for cyclic systems

Now that Putin can be blamed, all the inflation that the Western central banks have created with money printing (that they have under-reported) can now be reported. And that provides the cover for them to raise rates, to tackle these Putin Price Hikes.

But they certainly don’t want the blame for the resulting crash.

Or do they?

National governance is being seen to fail.

What if national central banking is seen to fail too?

Who would we turn to?

So if I am getting this straight, and I’m not sure if you’re watching this thread anymore (I wouldn’t blame you, being so busy) the RCB has started buying gold at a negotiated rate because there is a high demand for rubles in the Russian economy, so RCB has to lower rates and allow commercial banks to make loans to help adjust the Russian economy to the new sanctions economy which will inflate (a positive, helpful level of inflation) the Ruble supply and therefore gold will be bought at a negotiated rate for the time being while the Ruble supply is inflated to allow for increased economic activity and once this process stabilizes they will likely go back to selling commodities at a discount for gold? Or is this a cope?

“Broadly speaking, when the Fed raises rates and it causes a drain on the eurodollar system, it puts upward pressure on LIBOR. If Europe’s banks are more exposed to a rise in the cost of dollars then LIBOR should blow out faster than the Fed raises rates.”

I am understanding ‘blow out’ to mean deflate, is that correct?

dramatic rise in rate == blowout

Surely if the Russian President is confident that the demilitarization of Ukraine can be effected within a month, then he is expecting the dollar to be crashed within this time period. I can only surmise then that the Glaziev plan is just that, to create a short run on gold and silver, which will crash the dollar.

Fascinating comments and article. Thanks for posting Tom.

I’ll admit I don’t understand the minute details as Tom does, but….

My guess is they get a few rate hikes in before either another ‘medical event’, cyber attack, or whatever Davos wheel of fortune lands on and it conveniently allows them public approval to cut the hikes back. Throw in famine, civil unrest, massive inflation, shortages and probably lockdowns along with more QR code slavery passes to spice it up. Oh yes and all while the pedal is to the floor going ahead into the crack up boom we will see within 12-36 months.

Thoughts Tom ?

So if the national currencies were all, like the CAD, named after their Premier, what would the other currencies be called?

The Zombie, The Heffalump, The SpaceNazi, and the Seppuku?

The bottom line is this: it has to do with what people value. Some people value truth, honor, dignity, compassion, courage, and love more than they value money and others value money more than those other six words. Each of us values one side one more than the other. Right now and maybe it’s always been this way, too many of us seem to value money more. When and if that ever changes I wonder what we will talk about. Until then I admit I do appreciate these discussions. So thanks.

That is as close to a perfect description of the problem of humanity as anyone can put it. I think it boils down to empathy; and a lot fewer people have empathy, or they have it to a much smaller amount than is generally agreed upon in the field of psychology. The vast majority of all humans have little to no empathy, either that or other motives override their empathy and drive their decision making process and behavior. How else could anyone explain the world we have and have always had? It’s much easier to blame a relatively small number of elite bogeymen that control the world, rather than come to the actual nasty realization of why human society is the way it is. Sure those bogeymen exist, are usually always extremely wealthy, and are they beyond evil, but they would have no power at all were it not for the bulk of mankind.

Hi Tom,

You might want to spend a few minutes looking at this. I can’t vouch for the source or the translation or how much of it is nonsense. These things usually get leaked by the Epoch Times, so I am guessing that might be the source:

A Chinese general sees a ruthless America striving to contain his nation’s growth

https://fabiusmaximus.com/2015/10/21/qiao-liang-sees-china-vs-america-90041/

This was written in 2015, but go to the 10th paragraph… “Where else did they target? Ukraine, the connection between the EU and Russia.”

I don’t know if there is a Qiao Liang or a “dollar cycle” as he presupposes, but we did go from: “Now, It Is Time to Harvest China” to “Now, It Is Time to Harvest Europe” … so if he does exist, it is amazing how he called this. IMHO

Just another potential data point for your collection.

How do you see the back end of April panning out Tom? Is there a treasury report coming out the 20th? Regarding Le Pen, never say never – there’s still things that can happen in the next 12 days, and just because virtually all the French politicains are now tearing off their humanoid face masks and revealing the Schwabian family likeness, (is it the scaly skin or pterodactyl beak?), it doesn’t automatically mean the voters will acquiesce. It’s a redux of 2017, but as I said to the rather attractive gilet jaune at the Spanish border, (17.11.2017), “You did have a choice”. “No we didn’t!” she protested.

Hopefully they are older and wiser now and will protest better this time.

I don’t think Europe ever controlled the Eurodollar market, at its infancy it was controlled by the City of London‘s participants, but later – at least from the 1980ties on it became a fully self organizing creature – a swarm with some kind of swarm intelligence attached. I agree that there is a global fragmentation going on and the US will try to go it alone using the Dollar as a multipurpose weapon as well to undermine the EURO (hopefully successful) subdue the Yen (assisted by the insane BoJ) and put maximal stress on China via the Yuan and else.

I’m doubtful of how well Russia will thrive after becoming expelled of the international financial System